You're probably here because you've already heard the frustrating answer: laser hair removal is “cosmetic,” so insurance won't cover it.

But your situation may not feel cosmetic at all. If you're dealing with painful folliculitis, hair growth tied to a diagnosed hormone condition, or hair removal as part of gender-affirming care, the issue isn't vanity. It's daily distress, repeated skin irritation, or treatment that supports a medically recognized diagnosis. That difference matters.

Insurance companies still deny many of these requests. A policy review found that 47% of carriers had broad cosmetic exclusions for hair removal, yet 12% did cover facial hair removal when medical-necessity criteria were met (review of insurer medical policies). That's the key point: coverage is inconsistent, but it isn't impossible.

Patients often lose coverage opportunities because they ask the wrong question. They ask, “Does insurance cover laser hair removal?” The better question is, “Can my doctor document why this treatment is medically necessary under my plan?”

That's where the process changes. Approval usually depends less on the laser itself and more on diagnosis, chart notes, prior authorization, and how the claim is submitted. If you're considering treatment, it helps to understand both the clinical side and the paperwork side before you start. If you want the treatment overview first, laser hair removal at ProMD Health gives a general look at how the procedure works.

Table of Contents

- Introduction Why Your Cosmetic Problem May Be Medical

- The Critical Line Between Cosmetic and Medically Necessary

- Medical Conditions That May Qualify for Coverage

- How to Build Your Case for Insurance Coverage

- Step 1 Get the diagnosis documented correctly

- Step 2 Build a real letter of medical necessity

- Step 3 Confirm coding before anything is submitted

- Step 4 Submit prior authorization before treatment starts

- Step 5 Call the insurer with very specific questions

- Step 6 Keep your file organized like an appeal may be needed

- Navigating Denials and Exploring Alternatives

- Conclusion Taking Control of Your Treatment Journey

- Frequently Asked Questions

Introduction Why Your Cosmetic Problem May Be Medical

A patient comes in frustrated after years of shaving, waxing, and treating the same painful bumps over and over. Another is starting gender-affirming care and is told hair removal may be part of treatment, then hears “cosmetic” the moment insurance gets involved. Those cases do not start as vanity concerns in a clinic. They start as symptom, diagnosis, and treatment-planning problems.

Insurance decisions turn on documentation, not frustration.

That distinction matters because unwanted hair can sit inside a larger medical picture. Recurrent ingrown hairs, chronic folliculitis, irritation from constant shaving, and treatment requirements tied to another diagnosed condition may give a physician a reason to request coverage. The request still has to be built carefully. Insurers usually want a diagnosis, notes showing why hair reduction is part of treatment, and a record of what has already been tried.

This is why broad answers are not very helpful. Coverage for laser hair removal is uncommon, but some patients do have a path if the chart shows more than appearance alone. In practice, the strongest cases are the ones where the medical problem is clear before the claim is ever submitted.

Patients often ask whether their situation is “medical enough.” The better question is whether a doctor can document a condition, a treatment goal, and a reason laser treatment is appropriate for that specific case. If you are trying to understand how treatment is typically performed and documented in a clinical setting, this overview of laser hair removal treatment options gives useful background before you start the insurance process.

The goal here is to show the actual path for the small group of patients who may qualify, including what records to gather, what insurers look for, and how to respond if the first answer is no.

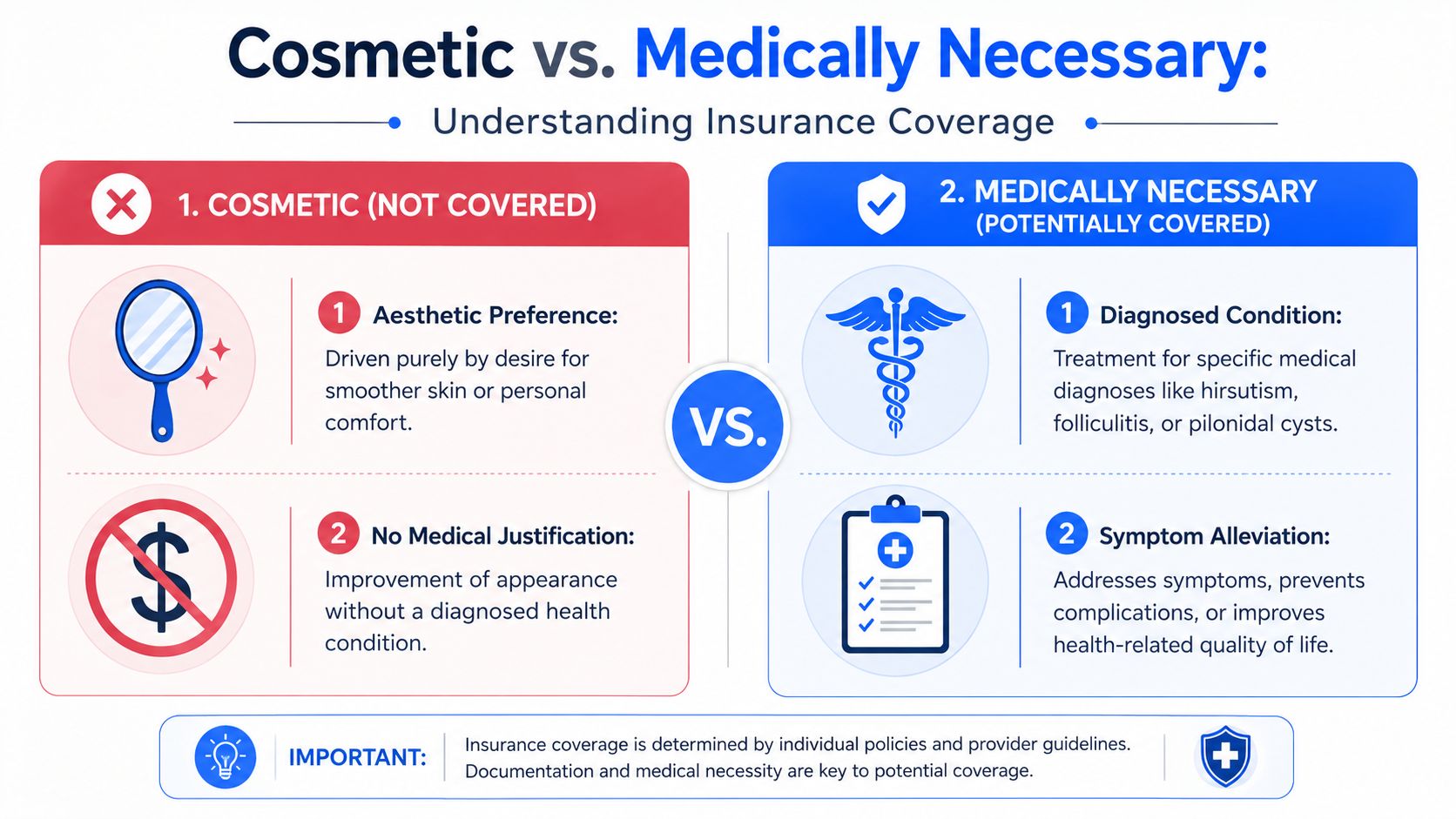

The Critical Line Between Cosmetic and Medically Necessary

A patient sits in my office with a real problem. Shaving triggers painful bumps. Waxing tears up the skin. The hair growth is tied to a diagnosed condition, but the insurance card in their wallet does not care about frustration alone. The reviewer wants to know a narrower point. Is this treatment addressing a documented medical issue, or is it being requested for appearance?

That distinction decides almost everything.

What insurers usually call cosmetic

Insurers usually place laser hair reduction in the cosmetic category if the chart describes convenience, grooming preference, or appearance goals. A claim also tends to fail if treatment begins before any prior authorization request, or if the record does not show a diagnosis, related symptoms, and earlier treatment attempts.

In practical terms, these cases are weak:

- Appearance is the stated goal: The notes focus on smoother skin or less grooming.

- The chart is too thin: There is no diagnosis tied to the hair growth or the skin complications it causes.

- Conservative care is missing: The record does not show what has already been tried and why it was not enough.

- The process starts in the wrong order: Sessions are scheduled before the insurer has reviewed the request.

I see this mistake often. The medical issue may be real, but the submitted file reads like a personal preference request.

What can move a case into medically necessary territory

Reviewers are looking for clinical purpose. They want to see that reducing hair is part of treating symptoms, preventing repeat skin injury, or supporting care for an established condition.

A stronger submission answers very specific questions:

| Insurance question | Stronger answer |

|---|---|

| Why is hair removal needed? | It is being used to reduce documented symptoms or support an active treatment plan |

| Who diagnosed the condition? | A licensed clinician documented findings in the chart |

| What has already been tried? | The record shows prior treatments and why they were inadequate |

| Why this treatment? | The provider explains why laser treatment fits this case medically |

| Was approval requested first? | Prior authorization was submitted before treatment started |

That is the line. Medical necessity is rarely about the device itself. It is about the diagnosis, the symptom burden, the failed alternatives, and the provider's written rationale all matching each other.

The part patients often miss

Patients often search for a list of qualifying diagnoses and assume the name of the condition will decide the outcome. In practice, the reviewer is reading a packet, not just a diagnosis code. If the chart does not connect the condition to a treatment goal, the request weakens fast.

Coverage for laser hair removal is less about the procedure and more about the documentation chain behind it. A good file shows cause, effect, and reason for treatment in a way an insurer can follow without filling in the gaps.

Medical Conditions That May Qualify for Coverage

Some diagnoses have a stronger path than others. The common thread is that the hair removal serves a medical function, not just a cosmetic one.

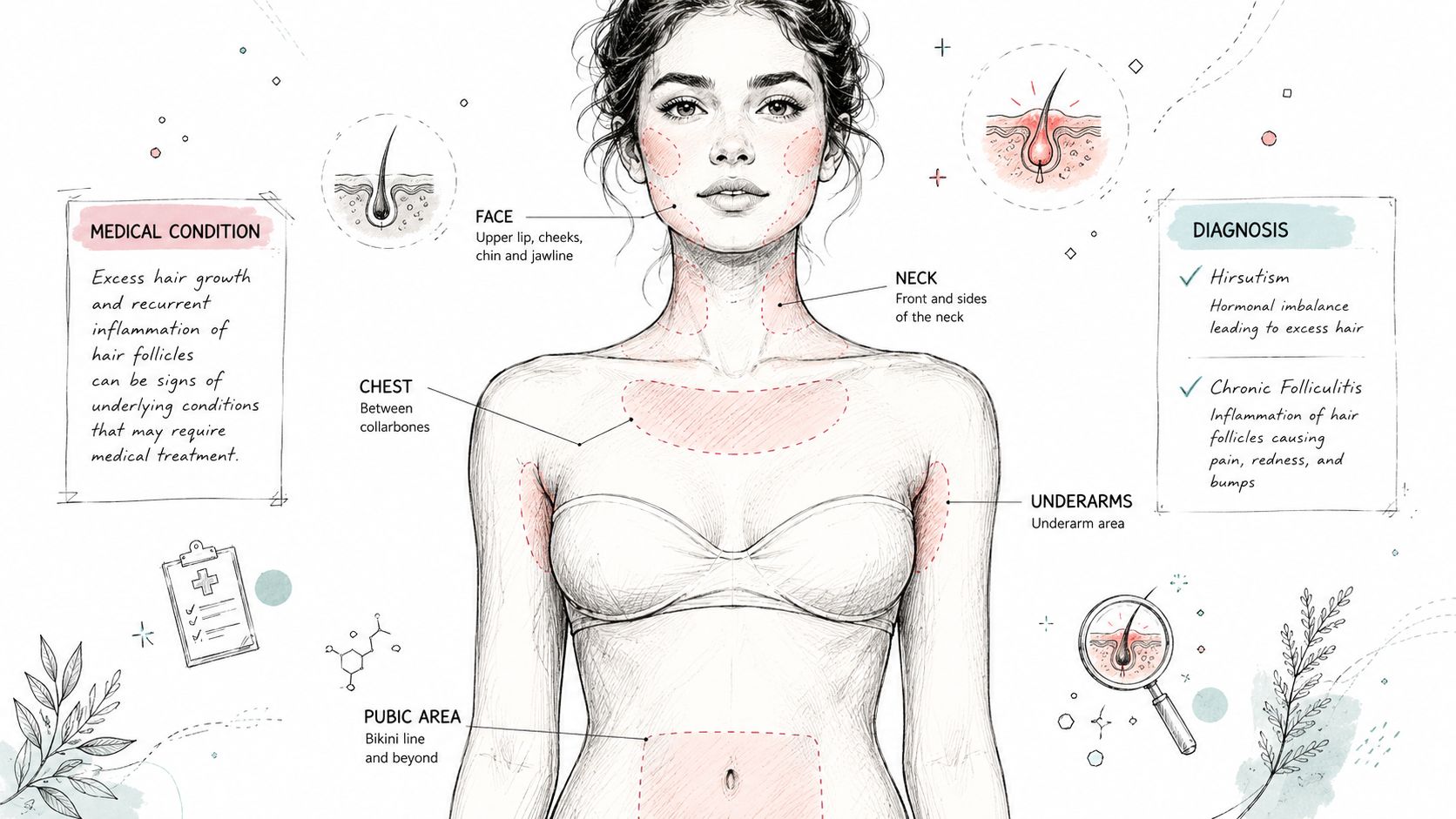

Hirsutism and hormone-related excess hair growth

Hirsutism is one of the first conditions patients mention, and for good reason. When a clinician documents abnormal or distressing hair growth tied to an underlying endocrine issue, the medical argument is stronger than it is for routine cosmetic treatment.

Still, many requests often fail for this reason. The diagnosis may be real, but the submission often lacks the operational details insurers want. The record has to show more than “patient bothered by hair.” It should connect the symptom to a medical condition and explain why laser treatment is part of management rather than preference.

A stronger chart usually includes:

- A formal diagnosis: The clinician identifies the underlying condition or symptom pattern.

- Clinical impact: The notes describe ongoing distress, skin problems, or other treatment-related burdens.

- Treatment rationale: The provider explains why laser is being recommended now.

Chronic folliculitis and related skin complications

This category can be compelling because the goal isn't beauty. It's reducing recurrent inflammation, ingrown hairs, or repeated infection risk in hair-bearing areas.

When I review these cases from a clinical operations perspective, the strongest files usually show repetition. One isolated episode of irritation rarely carries much weight. Recurrent symptoms, repeated office visits, failed topical or oral management, and persistent flare patterns are what make the request look medical.

Hair removal becomes easier to defend when the chart shows that hair itself is contributing to a recurring skin problem.

Conditions that may fit this pattern include chronic folliculitis and other hair-driven inflammatory problems where reducing the follicle burden is part of symptom control.

Gender-affirming care

This is often the clearest evidence-based pathway because documentation standards are more explicit than they are in routine cosmetic cases. For gender-affirming care, approval often depends on correct coding, including ICD-10 code F64.9 for gender dysphoria alongside the appropriate procedure code. Some clinics also note laser code 17999 and electrolysis 17380 as part of certain submissions. In one published clinic policy review context, 10% of carriers may consider coverage through a medical-necessity appeal even without explicit gender-dysphoria benefits in the plan (insurance workflow details for gender-affirming hair removal).

That doesn't mean approval is easy. It means the pathway is more defined.

A strong gender-affirming submission usually includes:

- Documented diagnosis: The clinician records the diagnosis clearly.

- Treatment plan linkage: Hair removal is shown as part of a broader care plan.

- Code accuracy: The diagnosis code and procedure code need to align.

- Pre-service review: Prior authorization is handled before treatment begins.

Cases that may be considered but need careful framing

Patients often ask about conditions such as PCOS, pilonidal disease, hidradenitis-related hair-bearing areas, or hair problems related to reconstructive or post-treatment care. These can be legitimate discussions, but the success of the request depends on how specifically the clinician documents the medical purpose.

In such cases, a broad internet list doesn't help much. The better question is not “Is my diagnosis on a list?” It's “Can my treating clinician explain why reducing hair is necessary to manage this condition under my plan's criteria?”

How to Build Your Case for Insurance Coverage

This is the part that most articles skip. They tell you to “get documentation,” but they don't explain what a usable insurance file looks like.

The operational approval path usually includes a formal diagnosis, a detailed letter of medical necessity, a prior authorization request, and correct billing codes. That process is described directly in this overview of medical-necessity documentation and insurer requirements. If you're trying to get laser hair removal covered by insurance, this is the core work.

Step 1 Get the diagnosis documented correctly

Start with the clinician who manages the condition. That may be a primary care physician, dermatologist, endocrinology provider, surgeon, or another licensed clinician depending on the case.

What matters is specificity. “Unwanted hair” is weak documentation. A diagnosed condition tied to symptoms or treatment goals is much stronger.

Ask for chart notes that clearly state:

- The diagnosis

- The symptoms or complications

- Why hair removal is being considered

- Why the issue is not purely cosmetic

Step 2 Build a real letter of medical necessity

A strong letter of medical necessity is not a one-line note. It should read like a clinical argument.

The best letters usually include these elements:

Patient history

The provider outlines how long the problem has existed and how it affects daily function, skin health, or treatment goals.Diagnosis support

The letter names the diagnosis and references the clinician's evaluation and records.Prior treatment history

If medications, topicals, hygiene measures, or other conservative approaches were tried, that should be documented.Reason laser is appropriate

The clinician explains why laser hair reduction is the next medically appropriate step.Requested service details

The insurer needs to know what is being requested, for which area, and under what diagnosis.

Documentation rule: The insurer should be able to understand the case without calling your doctor's office for basic clarification.

Step 3 Confirm coding before anything is submitted

Coding mistakes sink good cases.

For gender-affirming care, the coding pathway may involve F64.9, and some submissions use 17999 for laser hair removal or 17380 for electrolysis when appropriate to the plan's process, as noted earlier in this article. Other diagnoses require their own coding logic. The point is not to guess.

Have the treating office and the treatment office confirm:

- Which diagnosis code is being used

- Which procedure code will be submitted

- Whether the plan requires a modifier, attachment, or narrative

- Which provider should submit the authorization

Step 4 Submit prior authorization before treatment starts

This step is where many patients get tripped up. Even a medically supportable case may be denied if treatment begins before preapproval is on file.

A clean prior authorization packet often includes:

- Clinical notes

- Letter of medical necessity

- Supporting diagnosis documentation

- Relevant photos if the office uses them and the plan permits them

- The proposed treatment plan

- Correct diagnosis and procedure codes

If you want a patient-friendly overview of treatment logistics before starting, this clinic laser hair removal guide is useful for understanding how appointments and planning typically work.

Step 5 Call the insurer with very specific questions

Don't ask, “Is laser covered?” That often gets you a generic no.

Ask these instead:

- Is this service excluded when submitted under my diagnosis?

- Do you require prior authorization before the first session?

- Should the request come from the treating physician, the laser clinic, or both?

- What documents are required for medical-necessity review?

- If denied, what is the appeal route?

Take notes. Write down the date, time, representative name, and reference number if one is provided.

Step 6 Keep your file organized like an appeal may be needed

Even strong requests can be denied on the first pass. Patients who do best usually keep a simple record with every chart note, submission, insurer letter, and call summary in one place.

That preparation matters because an appeal often succeeds or fails based on whether the second review gets a cleaner, better-supported file than the first one did.

Navigating Denials and Exploring Alternatives

You submit the request, wait two weeks, and get a denial that says “cosmetic.” Patients often read that as the end of the road. In practice, it usually means one of two things. The plan excludes the service, or the reviewer did not get a file that clearly connected the treatment to a covered medical problem.

Read the denial letter like an insurance reviewer would

Start with the exact denial language, not your memory of the phone call. Look for the stated reason, any denial code, the date of the decision, the deadline to appeal, and whether the plan offers only an internal appeal or also an external review.

Those details tell you what can be fixed.

A practical review usually looks like this:

| Denial reason | What to check next |

|---|---|

| Cosmetic exclusion | Whether the policy excludes laser hair removal under all circumstances or only for appearance-related use |

| No medical necessity | Whether the records clearly tied the treatment to symptoms, recurrence, functional problems, or failed conservative care |

| No prior authorization | Whether approval was required before the first session and whether the request was sent to the correct department |

| Coding issue | Whether the diagnosis and procedure coding matched the chart notes and the authorization request |

The trade-off is simple. Some denials are paperwork problems. Some are plan-language problems. Paperwork problems are often worth fighting. A clear plan exclusion is harder to overturn unless the insurer applied the wrong benefit rule.

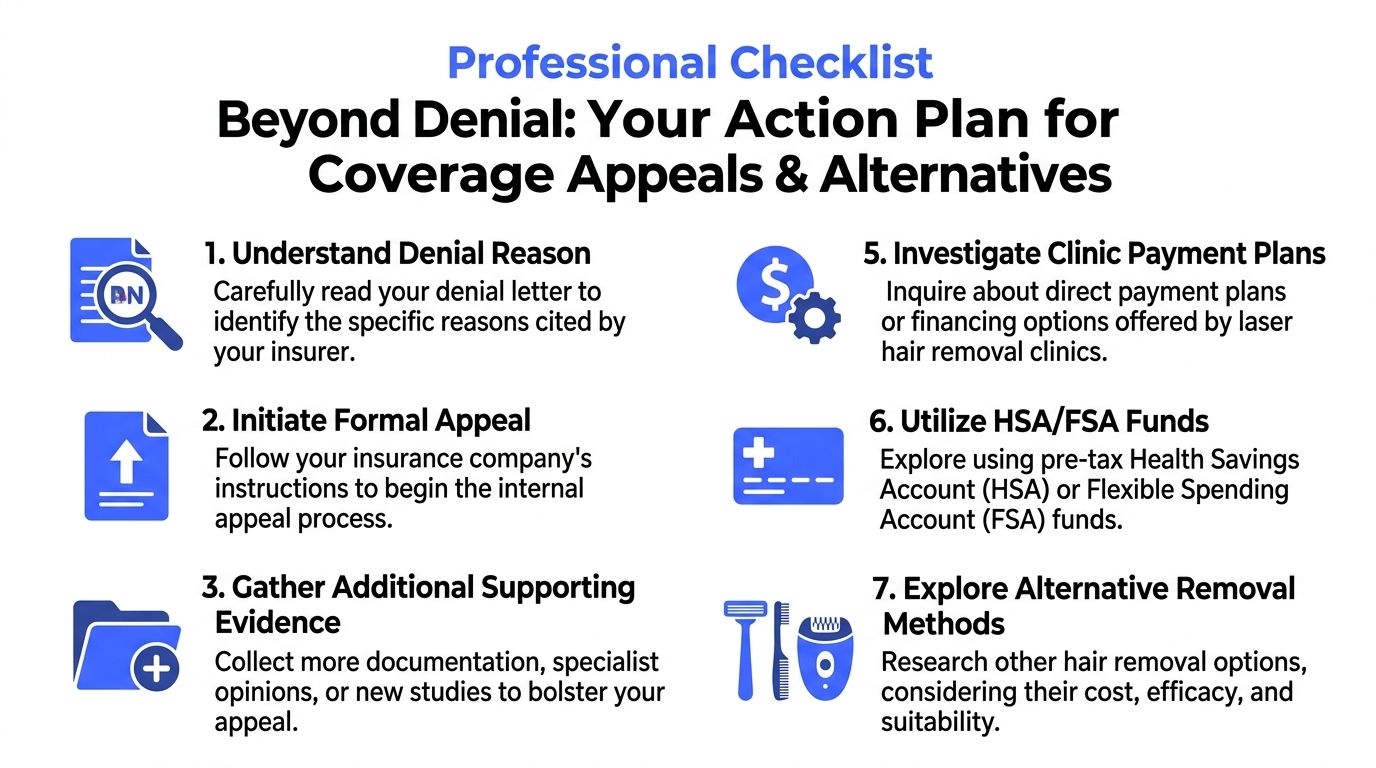

Appeal with a corrected file

An appeal works best when it answers the denial line by line. If the reviewer said the service was cosmetic, the appeal should point to the diagnosis, the symptoms, and the medical reason the hair itself is part of the problem. If the reviewer said there was no prior authorization, the office should confirm whether authorization was requested, whether it was misrouted, or whether the service date came before approval.

For patients who want a consumer-friendly overview of the appeal process itself, this expert guide on health insurance denials is a useful reference.

What usually improves an appeal:

- A revised medical-necessity letter that addresses the denial reason directly instead of repeating the original request.

- Clearer chart notes showing the condition, symptoms, prior treatment attempts, and why hair removal is part of treatment rather than preference.

- Coding review so the diagnosis, authorization request, and claim all match.

- A policy excerpt when available, especially if the plan covers treatment tied to a diagnosed condition but the first reviewer treated it as cosmetic by default.

One practical rule matters here. Do not resend the same packet.

If the internal appeal fails, read the denial notice again. Many plans explain whether you can request an independent external review and how quickly that request must be filed.

When coverage is not available

Sometimes the insurer's answer holds up after review. That is common when the plan excludes laser hair removal as a benefit category, even if the patient has a real medical complaint. In those cases, the conversation shifts from coverage strategy to cost strategy.

Laser hair removal usually requires multiple sessions, and cosmetic claims often leave the patient responsible for the full bill. That matters because a treatment plan that is medically helpful can still become unrealistic if the out-of-pocket cost is too high all at once.

Patients usually consider a few options:

- Clinic payment plans to spread out the expense over time.

- HSA or FSA funds if the account rules and supporting documentation allow it.

- Treating the highest-burden area first when symptoms are concentrated in one region.

- Temporary alternatives if the full laser plan is not affordable right now.

If you are comparing out-of-pocket options, ProMD Health financing offers show the type of payment resource many patients review when insurance approval does not come through.

The goal is not to chase approval forever. The goal is to decide, with good information, whether this is a fixable denial, an appealable denial, or a noncovered service that needs a realistic payment plan.

Conclusion Taking Control of Your Treatment Journey

The biggest mistake patients make is treating insurance approval like a mystery. It usually isn't. It's a paperwork and policy problem that has to be approached in a very specific way.

Laser hair removal covered by insurance is limited to narrow circumstances, but those circumstances are real. The strongest cases have three things in common: a formal diagnosis, documentation that explains why treatment is medically necessary, and a complete prior authorization process before treatment starts.

If you're denied, don't assume the answer was clinically final. Review the reason, tighten the file, and appeal when the facts support it. If you want a practice-side view of how denied claims are often challenged, Happy Billing's guide for medical practices is a helpful resource because it shows how denial responses are built from the documentation side.

Patients who do well in this process stop thinking like shoppers and start thinking like advocates. Ask for the diagnosis in writing. Ask for the letter of medical necessity. Ask which codes are being used. Ask whether prior authorization has been approved. Those questions often make the difference.

Frequently Asked Questions

Does Medicare cover laser hair removal

Usually no, because cosmetic procedures generally aren't covered. Coverage may only be considered in limited medical situations, and plan-specific review still applies.

Is laser more likely to be covered than electrolysis

Not necessarily. In gender-affirming care especially, the answer depends on the plan, the treatment purpose, the procedure stage, and the coding used. Claims can be denied even when coverage exists if prior authorization is missing. That pre-service workflow often involves specific CPT and ICD-10 coding plus a detailed treatment plan, as discussed in this guidance on gender-affirming hair removal reimbursement.

Can I use HSA or FSA funds

Sometimes, but don't assume. For medically necessary care, patients often need supporting documentation such as a letter of medical necessity, and account rules still apply.

What's the single biggest reason claims fail

In practice, it's usually weak documentation or skipped preauthorization. A legitimate diagnosis helps, but it won't carry the claim by itself.

Should I start treatment before approval comes through

No. If your plan requires prior authorization, starting first can create a denial problem that is much harder to fix later.

If you're trying to sort out whether your case has a real insurance pathway, ProMD Health offers laser hair removal along with consultation and treatment-planning support, which can help you evaluate both the clinical fit and the financial path before you begin.